ICON TEAM

KIMBERLEE RANDALL GROUP

Serving MD, DC, VA, and PA

Meet Kimberlee Randall

Kimberlee Randall is an esteemed real estate agent with over 15 years of experience in the real estate industry. Known for her exceptional leadership skills, unwavering dedication, and passion for client satisfaction, she has established herself as a prominent figure in the field. In 2019, Kimberlee founded the Kimberlee Randall Group, marking a significant milestone in her career. The establishment of the Kimberlee Randall Group in 2019 further solidified her position as a leader in the field.

Throughout her extensive tenure in real estate, Kimberlee has consistently showcased her expertise and commitment to excellence. Her deep understanding of the industry, coupled with her unparalleled work ethic, has allowed her to thrive in various market conditions. Her wealth of experience provides her with valuable insights and a keen ability to navigate complex transactions, ensuring optimal results for her clients.

Explore Our Tailored Resources

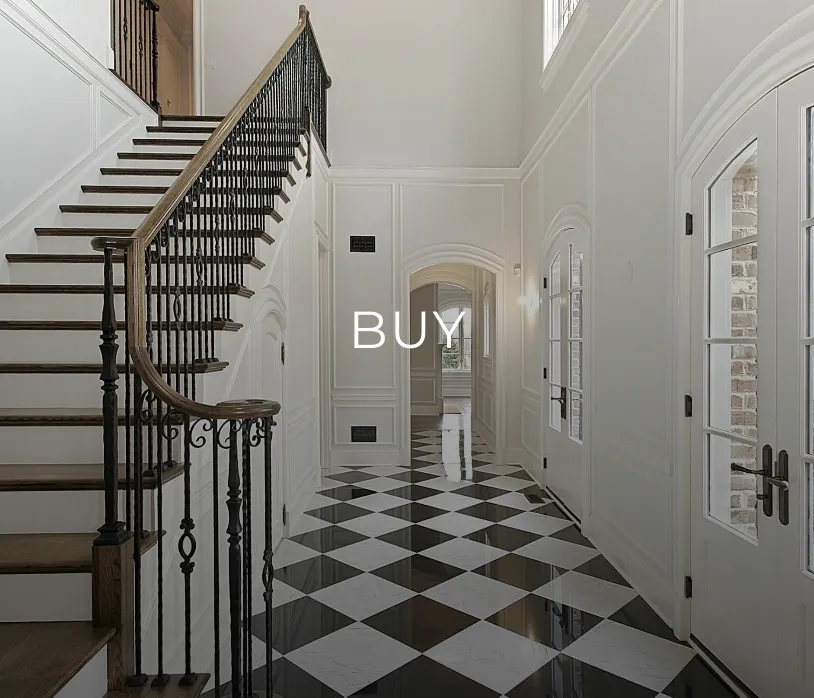

Your Comprehensive Home Buying Blueprint

Our comprehensive resource center provides a wealth of helpful tools and detailed guides tailored to the coastal market. Use our investment calculators, including the ROI and mortgage calculators, to run scenarios on properties in MA, VA, DC, or PA.

We give you the exact knowledge and resources required to execute your home buying plan with total confidence, turning strategy into sustained, stress-free success.

Curious about your home's value?

EXPLORE NEIGHBORHOODS

Testimonials

Here are some of our client success stories

I cannot recommend Kim, Alexeus and Kristina enough. Their professionalism, efficiency and passion is unmatched. Communication was consistent and transparent, and it was clear that their clients always come first. They made my first home buying experience incredible.

The team’s communication is outstanding. Kimberlee and Alexeus consistently demonstrate strong negotiation and problem solving skills, and Kristina ensures everything stays on track. Their teamwork makes every transaction seamless.

Working with Kimberlee was a game changer. Her marketing and negotiation skills helped us go under contract in less than two weeks and above asking price. Her team was responsive and professional throughout.

As a first time home buyer, the process could not have been smoother. Alexeus was knowledgeable, responsive, and made me feel confident at every step. She truly cares about her clients.

Kim is extremely professional and efficient. She ensures you find exactly what you need and has trusted contacts for everything related to your home. Truly a one stop resource.

Kimberly was amazing. She answered every question thoroughly and made the process smooth and stress free. We closed within one month thanks to her dedication.

I cannot recommend Kim, Alexeus and Kristina enough. Their professionalism, efficiency and passion is unmatched. Communication was consistent and transparent, and it was clear that their clients always come first.

The team’s communication is outstanding. Kimberlee and Alexeus consistently demonstrate strong negotiation and problem solving skills, and Kristina ensures everything stays on track.

Working with Kimberlee was a game changer. Her marketing and negotiation skills helped us go under contract quickly and above asking price.

As a first time home buyer, Alexeus made the process smooth and enjoyable. She truly cares about her clients.

Kimberlee Randall

📍Serving the DMV + PA | Hablamos Español.

🔑 3X ICON REAL ESTATE TEAM

⭐️TOP 15% Teams by Homes.com

Dedicated, passionate guidance for all your real estate needs.

With deep expertise across Washington DC, Maryland, Virginia, and Pennsylvania, Kimberlee delivers strategic, personalized guidance tailored to your unique goals. Connect with the Kimberlee Randall Group today and work with a trusted, results driven real estate team committed to helping you move with confidence and success.